Business

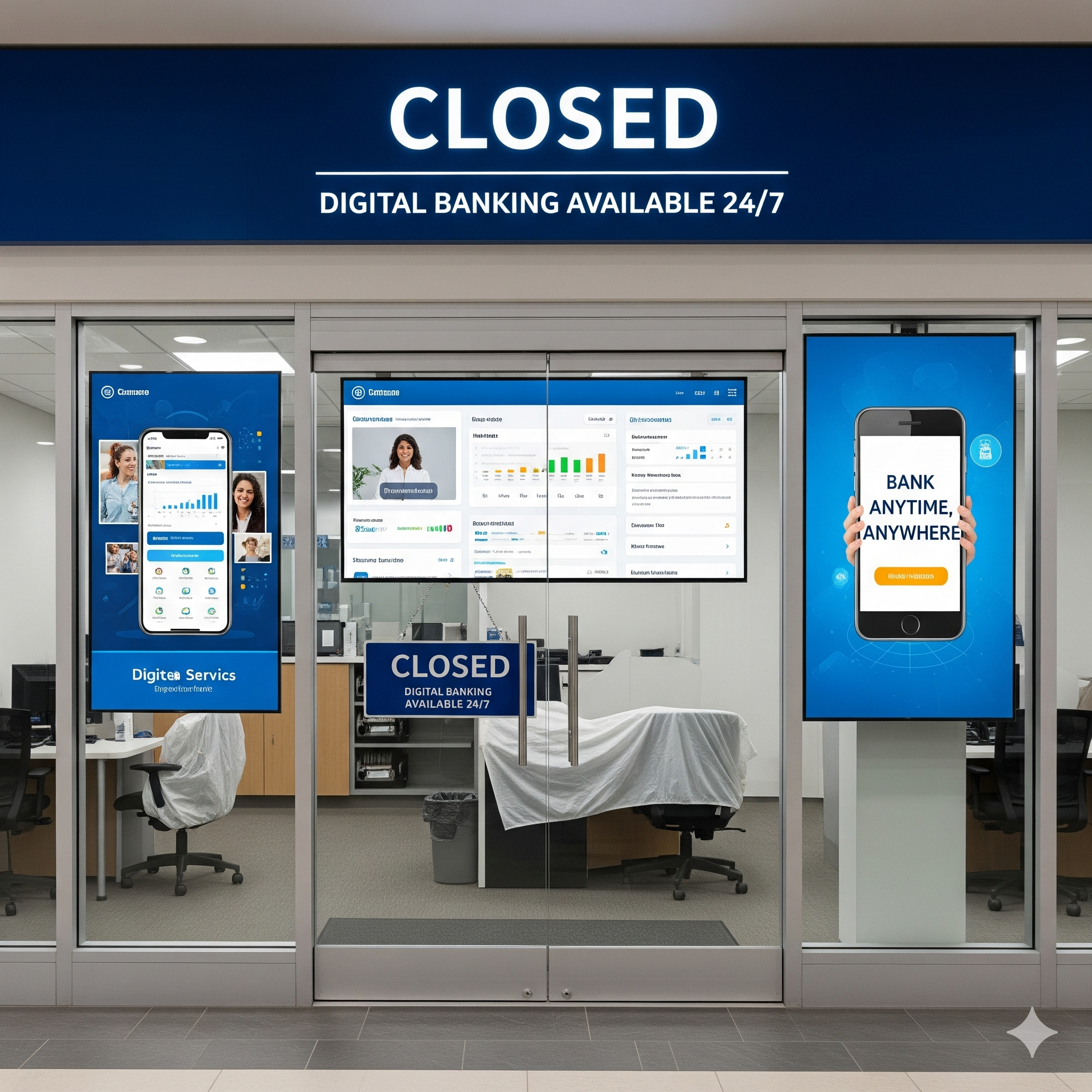

As digital banking becomes the norm, U.S. banks are closing physical branches at an accelerating pace, reshaping how people access financial services. This trend affects deposit habits, community banking, and the future of checking accounts and in-person support.

A recent analysis shows that since 2020, U.S. banks—including giants like Wells Fargo, JPMorgan Chase, and Bank of America—have shuttered 5.6% of physical branches. This shift stems from growing reliance on mobile apps and online services like checking accounts and digital wallets.

Digital banking enables convenient access to deposits, checking accounts, loans, and mortgage applications from anywhere. It suits tech-savvy users—but for seniors, underbanked communities, or those who prefer face-to-face service, branch closures can mean reduced access. In areas with few remaining branches—so-called “banking deserts”—residents may struggle to open deposit accounts, negotiate loans, or handle complex financial matters.

Cutting branches helps banks reduce operating costs and reallocate resources to digital innovation—like AI-powered customer support or video teller ATMs. These moves enhance efficiency and align with consumer preferences. However, ensuring financial inclusion remains essential. Many banks are exploring hybrid solutions such as mobile branch buses and expanded digital support to fill service gaps.

The branch closure trend reflects a long-term transformation: from in-branch service toward digital-first models. While this transition improves cost structure and convenience, it may exacerbate inequities in financial access. Addressing this requires thoughtful strategies—like maintaining baseline physical presence in underserved areas, while boosting digital literacy and secure digital alternatives.

Closing Insight

Branch closures offer efficiency and reflect consumer preferences—but banks and regulators must balance innovation with equitable access, ensuring no one is left behind.

Closing Insights

Economic Insight: Consolidating branches supports margins, but sustainable growth demands accessible digital alternatives for all demographics.

Professional Tip: Consumers interested in loans or mortgages should explore digital offerings—but also confirm digital support options, especially for complex services.

Looking Ahead: Hybrid models combining digital tools and physical access points may define the next era of inclusive banking.

Previous Post

Previous Post Israel’s Banks Offer Relief Amid Record Profits During Wartime

Next Post

Next Post Sygnum Expands Crypto Asset Management to Germany & Liechtenstein | Digital Banking Insights

April 28, 2026

April 28, 2026

April 28, 2026

April 28, 2026

SKN | Rupee Liquidity Tightening in India: What Central Bank Intervention Signals for Cross-Border Capital Positioning

SKN | Escalating Institutional Losses in European Clearing Banks: Implications for Custody, Liquidity, and Capital Security

SKN | Political Risk and Banking Tensions in Europe: What It Means for Cross-Border Wealth Stability

Optimized by Seraphinite Accelerator

Optimized by Seraphinite Accelerator